Vedanta’s demerger is a clean one, but leaves some questions unanswered

The demerger will see individual businesses find their true market value but how debt will be apportioned and how it will address the promoters’ debt challenge is unclear

On a day that the listed Vedanta announced its much-awaited demerger, S&P Global Ratings downgraded parent company Vedanta Resources' rating due to a prospective bond extension exercise. This is the context in which Vedanta's demerger is occurring, but it is not yet obvious how it will improve the parent company's funding profile. The process is anticipated to take 12 to 15 months, and Vedanta Resources' $2 billion in loans will mature in two tranches in 2024.

What proposals has Vedanta made? It will separate five operating businesses, including aluminum, oil and gas, base metals (primarily international copper and zinc), ferrous (steel and iron ore mining), and electricity. The sixth company will be Vedanta, which will continue to retain the Hindustan Zinc (HZL) stake and will also fund investments in new sectors including semiconducting and display.

Therefore, Vedanta will continue to operate as a holding company. Depending on whether or not Vedanta is the buyer after the government sells its stake in HZL, a second round of consolidation could occur. The current market capitalization of Vedanta is Rs 82707 crores, whereas its 65 percent stake in Hindustan Zinc is valued at Rs 84660 crores. In addition to a holding company discount, substantial debt on the balance sheet, promoters' debt issues, and difficulties in certain businesses may be dragging down its valuation. Therefore, it may actually benefit from a reduced balance sheet following the demerger, subject to the capital expenditure commitments of capital-intensive businesses such as semiconductors.

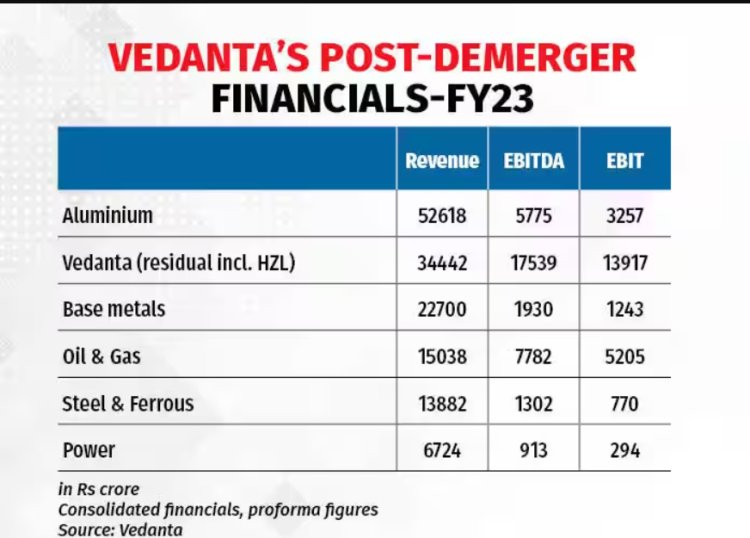

Aluminum is the largest demerged business by revenue and is also in a relatively robust position (see graph). The metal's long-term demand outlook is favorable, and Vedanta's plans to increase capacity and the proportion of value-added products should ensure that it remains a major contributor. The oil & gas business is a significant contributor to Vedanta's consolidated EBITDA, but it confronts obstacles in increasing its output, which may cause investors concern.

Vedanta's post-demerger financials-FY23

Vedanta initiated a strategic evaluation of the steel and ferrous company some time ago in order to consider an exit by selling Electrosteel Steel. According to reports, the transaction was stalled due to a steep asking price. Even if it is sold, Vedanta may still retain the iron ore mining business, which was earlier operated as Sesa Goa and is a large and very profitable business. In this instance, however, the iron ore mining operations in Goa have been disrupted, and until new mining leases are signed, this uncertainty will impact the output of this business.

The base metals company faces challenges as it will own the closed Tuticorin copper plant. Although Vedanta expects the plant to resume operations in 2024, the company's valuation depends on whether the plant resumes operations before it goes public. If it does not, it will probably languish.

The overhang of these underperforming businesses, which may be offsetting Vedanta's profitable or expanding businesses, will be eliminated following the demerger. Combining multiple enterprises was intended to provide a hedge, but in some cases it became a millstone. As things stand, the demerger should result in a significant realization of value in its aluminium business. It is crucial to examine how the debt is distributed among companies, as this will determine the amount of obligation that each company must service.

However, one major question persists. What are the benefits to the promoters? The urgent need is to ensure that sufficient funds are available to service Vedanta Resources' debt obligations not only in 2024, but also in the future, so that they do not face this problem again. Currently, it is unclear how this issue will be resolved, as nothing substantial has changed on that front. If it takes more than a year to conclude the demerger, where will the money come from besides the normal practice of paying dividends?

An increase in Vedanta's valuation can be advantageous if investors incorporate the anticipated release of value into Vedanta's current share prices. The company's stock price increased by 7% on September 29th, following news of the demerger. Since the promoters have pledged Vedanta's shares to raise capital, a higher market value will reassure lenders and, if the upward trend continues, provide the opportunity to raise additional funds.

Once the companies are split, if the sum of their separate valuations is significantly higher than the present valuation, the promoters' funding limits will be increased based on their individual holdings. Lastly, they have the option of selling one of these demerged entities and raising capital through a partial or complete exit. The proposed HZL demerger of its silver and recycling enterprises makes no sense unless they intend to sell their silver unit. Read further here.

A great deal hinges on what may prove to be the group's final gamble to surmount its debt-related difficulties and even for its minority shareholders to earn profitable returns.

Also read :- JSW Infrastructure, Vaibhav Jewellers advance listing date, to debut on October 3

.jpeg?updatedAt=1698674189520)